This is the third and final post in our three-part series on consumer financing solutions. This article discusses how to overcome objections to financing a sale.

Be sure to read our previous posts:

- Part 1: Common Reasons Why Businesses Offer Financing

- Part 2: What You Need to Know About Offering Consumer Financing

The road to closing a sale is rarely ever a linear one – for businesses and consumers alike – because questions and hesitations and necessary time to think a purchase through are common and important.

Sure, you’ve undoubtedly experienced transactions where there are little to no questions or back and forth, and business is quickly concluded. But, for the most part, sales and common sales objections walk hand-in-hand – necessitating honest but strategic sales closing techniques from you.

For products and services where consumers are on the fence because ‘the price is way too high,’ or ‘a competitor’s price is better,’ or ‘they’re weary about financing options’ (or any number of other consumer hesitations or objections), it’s imperative to understand common sales objections and the most effective ways to overcome them.

Common Sales Objections and Responses:

We’re certain you can come up with a long list of the common sales objections received throughout your years in sales. We’ve found that at the crux of most sales conversations, you’re likely to find one of these common objections. Below each is possible statements to overcome that objection:

- [Price Objection] “The price is too high.”

RESPONSE: “It may sound high, but the list price is quite competitive for the value our product provides.” - [Price Objection] “The price is too high. Is there any way you can come down a bit with your price?”

RESPONSE: “We feel the value of our product is reflected in the price. Keep in mind, you can finance the purchase and pay off the balance early to save on interest. And there is no early pay-off fee.” - [A Competitor is Cheaper] “I can get this [product or service] cheaper elsewhere.”

RESPONSE: “Be sure you compare the qualities of our product/service to the elsewhere you mention. Our service is impeccable and we stand behind our product.” - [Bad Timing] “I can’t afford this right now. We’re just not ready to buy”

RESPONSE: “We offer a low monthly payment plan, so you can make your purchase right away without paying an upfront cost, and then pay off your purchase over time.” - [Bad Timing] “We don’t have any budget left right now.”

RESPONSE: “We have a financing option, meaning low monthly payments. Rather than a credit card, it’s a set dollar amount for a set number of months. For the product you’re considering, it would be approximately $___ for __ months.” - [Stall or ROI Concern] “It’s just not important right now.”

RESPONSE: Here’s where a salesperson can ask questions that might lead to one of the topics above! Perhaps gauge why it’s not important right now and ask when it might be important. The salesperson can ask, “Can I reach back out to you in a few months?”

While in the process to strengthen your sales techniques and better understand objections, there is never a one-size-fits-all solution.

But have you considered how discussing financing options can help in overcoming price objections and truly help customers obtain the product or service they want or need?

Does Your Sales Process Offer Financing Options?

Offering a simple and straightforward financing option can make it easy for your customers to see that your services come attached to low monthly payments that align with their budget – which can put them at ease when trying to determine how to afford your product or service now, not wait for months or years to save their money.

Consumer financing is an influential tool that has the power to:

- Instill confidence in consumers

- Help consumers to better focus on the features, benefits and value of your products or services (rather than the price tag)

- Help consumers ignore options or proposals from your competition

- Help in overcoming price objections

- Help you maintain the full MSRP

- Help you from losing the sale altogether

Learn how you can grow your business and expand your customers’ payment options with one of the best financing options on the market today:

Sales Closing Techniques: How to Introduce Consumer Financing into Your Sales Conversation

Successfully overcoming price objections starts and ends with you acknowledging the customer’s concern while still furthering the conversation with helpful, advantageous insights and options.

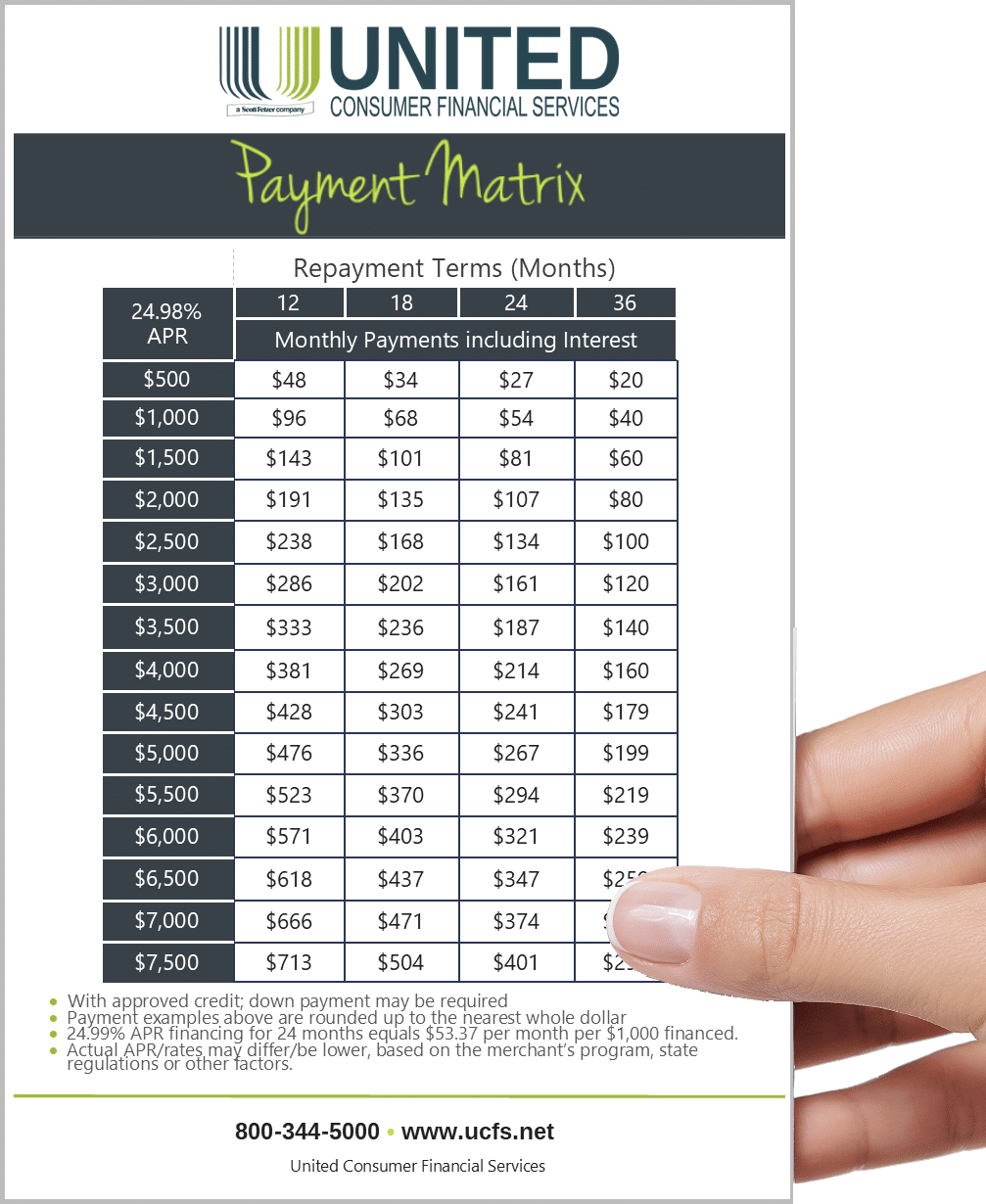

One of the best ways to do this is by telling customers a low monthly payment dollar amount. Offering an an alternate payment option helps customer visualize how they can make their purchase. Business customers are provided with a chart showing approximate monthly payment amounts for terms offered to help speed the conversation. Click here to see an example!

{kind=link}

To introduce consumer financing into your sales conversation, you can:

- State that “Financing Is Available” or list a specific low monthly payment offer on your website, phone message, sell sheets, and pricing proposals.

- Bring up financing early in the sales process and speak in terms of monthly payments.

- Include the low monthly payment dollar amount on every quote.

- Emphasize the monthly payment amount, instead of the product or service total price.

*UCFS provides templates with text and images to help businesses advertise low monthly payments on their website or in a PDF to print, post, or send by email.

Help Customers Obtain the Product or Service They Want or Need by Offering Financing Options from UCFS

When your financing partner is United Consumer Financial Services, even consumer objections like, “I don’t want another monthly payment,” and, “I don’t want to get stuck in a contract,” become easier to deflate because our program works in the best interest of your customers (and your business) and gives customers the best opportunity to repay.

As a leader in consumer financing who works with merchants and distributors to provide the best contracts and financing services available today, we work hard to help you meet customers’ needs and offer every customer a financing option that suits their budget – even customers with credit that is not optimal.

The low, fixed amount per month – with a set end date – helps customers completely pay off the cost of products or services on a term that has a lower impact on their daily financial commitment, especially as compared to revolving credit cards with even higher interest.

Let’s talk about how we can help you overcome common sales objections, learn new sales closing techniques and streamline and grow your business.

Learn more about partnering with UCFS or get in touch with us directly today: